April 15, 2026

·8 min read

How Much Should Your Emergency Fund Be? The Real Answer

The standard advice is 3–6 months of expenses. You've probably heard it. What you've probably not seen is the actual calculation behind it, the factors that should push you toward 3 or toward 6 (or beyond), and what most people get wrong about where to keep it.

This is the full picture.

Why the emergency fund exists

An emergency fund has one job: to prevent a financial shock from becoming a financial spiral.

Without one, a $1,500 car repair, a week of unpaid sick leave, or a broken appliance goes on a credit card at 20%+ interest. That single event can set back months of financial progress. Repeated enough times, it keeps people permanently behind — not because their income is too low or their spending is too high, but because they have no buffer between the unexpected and their debt.

The math is brutal in the other direction too. Bankrate's 2025 Emergency Savings Report found that more than half of Americans cannot cover an unexpected $1,000 expense from savings. One in five cannot cover $500. These are not people with catastrophically low incomes — they are people whose cash is tied up, spent, or simply never set aside.

The emergency fund is not an investment. It is not supposed to grow aggressively. It is insurance that pays you 100 cents on the dollar the moment you need it, with no withdrawal penalty and no paperwork.

The calculation: how to find your actual number

The 3–6 month rule is correct but incomplete without knowing what to multiply. The base is your essential monthly expenses — not your total spending, and not your income.

Essential expenses include:

- —Rent or mortgage

- —Utilities (electricity, gas, water, internet)

- —Groceries

- —Insurance premiums (health, car, renters/home)

- —Minimum debt payments

- —Transportation costs (car payment, fuel, or transit)

- —Any subscriptions or services you'd keep even if your income dropped

What you leave out: dining out, entertainment, clothing, vacations, non-essential subscriptions. In a genuine emergency, these would stop. Your essential expenses are the floor — what it costs to keep your life running at minimum.

Once you have that monthly number, the question is how many months to target.

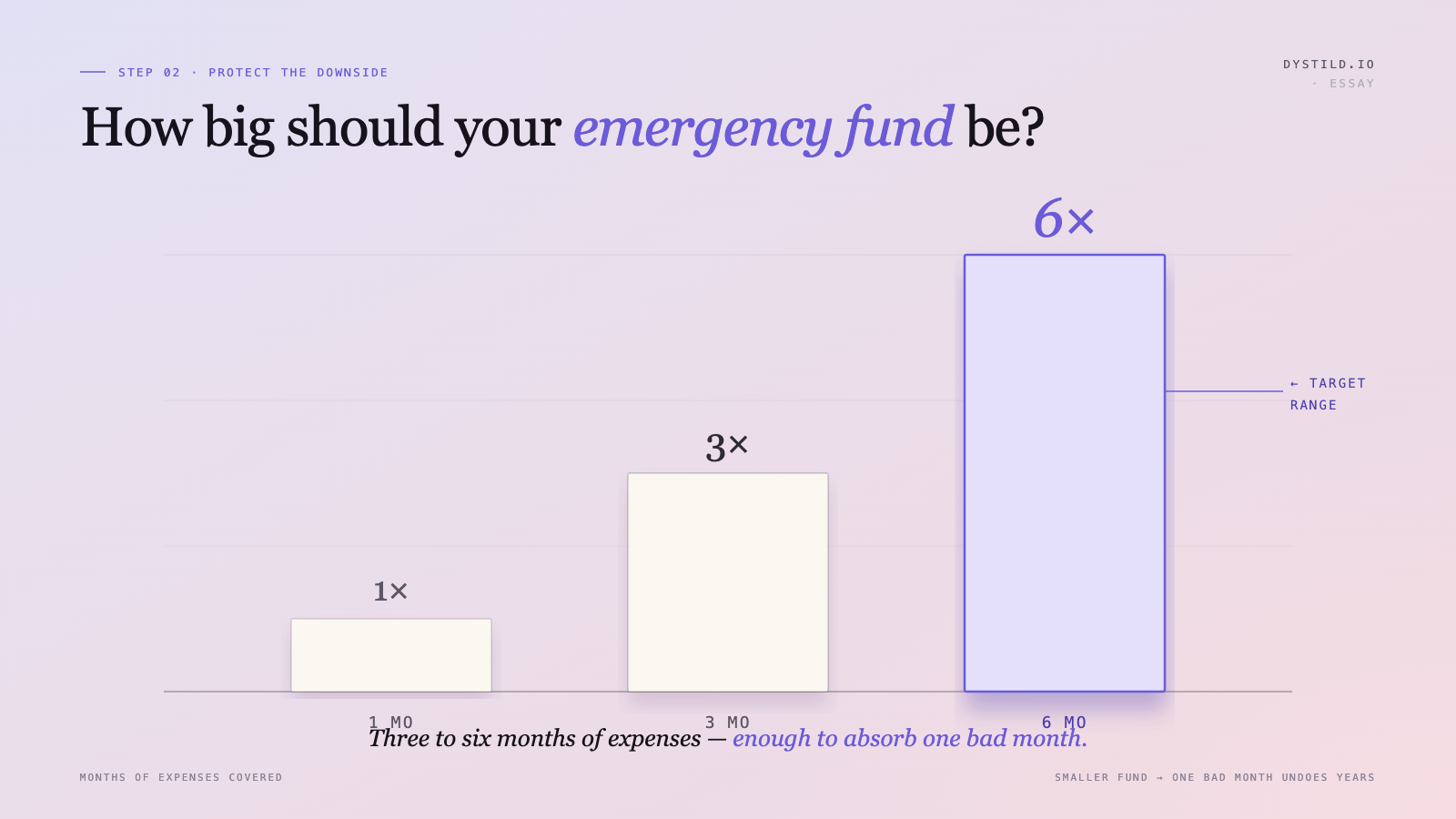

How many months you actually need

The 3–6 month range exists because different situations have genuinely different risk profiles.

Target 3 months if: - You have a stable salaried job with low industry volatility - You have a dual-income household — if one person loses their job, the other covers essentials - You have a strong financial safety net (family support you'd genuinely use, significant accessible investments) - You have low fixed expenses relative to your income

Target 6 months if: - You are a single-income household - You have dependents (children or others relying on your income) - You own a home (higher-ticket unexpected expenses — HVAC, roof, appliance replacements) - Your industry has periodic layoffs or your income is partially variable - You would feel significant anxiety with only 3 months saved

Target more than 6 months if: - You are self-employed or freelance — income can stop with no notice, and new income can take months to rebuild - Your field has long hiring timelines (finding a new job typically takes 3–6 months in many industries) - You have significant health considerations that could affect your ability to work - You are near or in retirement

For reference, a 2025 analysis based on US Census data found that the average American household needs approximately $35,000 to cover six months of essential expenses — roughly 40% of the average household's annual income. Yours may be higher or lower, but the order of magnitude gives a useful sense of what "funded" actually looks like.

The most common mistakes people make with emergency funds

Mistake 1: Keeping it in a checking account

This is the most widespread and most costly mistake. The money is there — but it is earning essentially nothing. A $20,000 emergency fund in a checking account at 0.01% earns $2 per year. The same balance in a high-yield savings account at 4% earns $800 per year. Over five years, that difference compounds to over $4,000 — real money left on the table for no reason other than not moving the account.

Your emergency fund should be in a high-yield savings account: liquid, FDIC-insured, and earning a real return on the balance while you (hopefully) never need it.

Mistake 2: Counting investments as emergency savings

A brokerage account, a 401k, or even a Roth IRA is not an emergency fund. The stock market can drop 30–40% in a recession — which is exactly when you're most likely to need emergency funds (job loss, reduced hours, unexpected expenses all cluster during downturns). Withdrawing from a 401k in an emergency triggers a 10% penalty plus income tax. Selling investments during a downturn locks in losses. Neither outcome is what emergency savings are for.

The emergency fund needs to be cash, or cash-equivalent. Accessible within 24–48 hours, with no penalty, no tax event, and no market risk.

Mistake 3: Raiding it for non-emergencies

An emergency fund is not a savings account you draw from when something expensive but predictable comes up. Car maintenance, holiday gifts, and annual insurance premiums are not emergencies — they are irregular expenses that should have their own savings category. Using the emergency fund for planned expenses means it is never actually funded when the genuine unexpected event arrives.

Mistake 4: Building it before eliminating high-interest debt

There is a hierarchy. If you carry credit card debt at 20%+, paying that down is a higher-priority return than building savings. The exception is a minimum emergency buffer — most financial planners suggest keeping $1,000 as a starter fund while aggressively paying down high-interest debt. Once the debt is cleared, build the full emergency fund. The logic: without any buffer, a single unexpected expense goes back onto the card, undoing all the payoff progress.

How to build it without it feeling overwhelming

The size of a fully funded emergency fund can feel daunting. $15,000 to $30,000 is not a number most people have lying around. The key is treating it as a target you build toward, not a threshold you have to clear before anything else matters.

A practical approach:

Start with $1,000. This covers the most common small emergencies — a car repair, a medical bill, a broken appliance. Having $1,000 available means those events don't go on a credit card. This is the first meaningful threshold.

Set an automated transfer. Decide on a monthly amount you can consistently move to your HYSA without noticing. Even $100 a month builds $1,200 per year. Automation removes the decision — the money moves before you have a chance to spend it.

Define your target number. Calculate your essential monthly expenses and multiply by your target months. Write the number down. Having a specific goal is meaningfully different from having a vague intention.

Treat windfalls as an accelerant. Tax refunds, bonuses, and any unexpected income should go partially toward the emergency fund until it is funded. Once it is fully built, those same windfalls can be redirected to investments.

Once it is funded: leave it alone

A fully funded emergency fund requires almost no ongoing management. You do not need to review it frequently, rebalance it, or add to it unless your expenses grow significantly.

The only meaningful action is to periodically check that the HYSA is still offering a competitive rate. Rates change. Banks quietly lower their APY over time, particularly if you've been a customer for a while. Checking once or twice a year and switching if the rate has dropped significantly takes 30 minutes and costs nothing.

The number that matters

Your emergency fund target is your essential monthly expenses multiplied by 3, 6, or more depending on your risk profile. It should live in a high-yield savings account, be treated as untouchable except for genuine emergencies, and be built before any significant investment activity beyond capturing your employer's 401k match.

If you do not currently have one, starting is more important than starting perfectly. $500 in a HYSA today is already more protection than $0.