April 7, 2026

·5 min read

The Free 50% Return Most People Are Ignoring

If someone offered you a 50% guaranteed return on an investment, you'd take it immediately. No questions. You wouldn't need to research the market conditions or think about your risk tolerance. A 50% guaranteed return is the best deal in finance, full stop.

Your employer match is exactly that, and about one in four people aren't taking it.

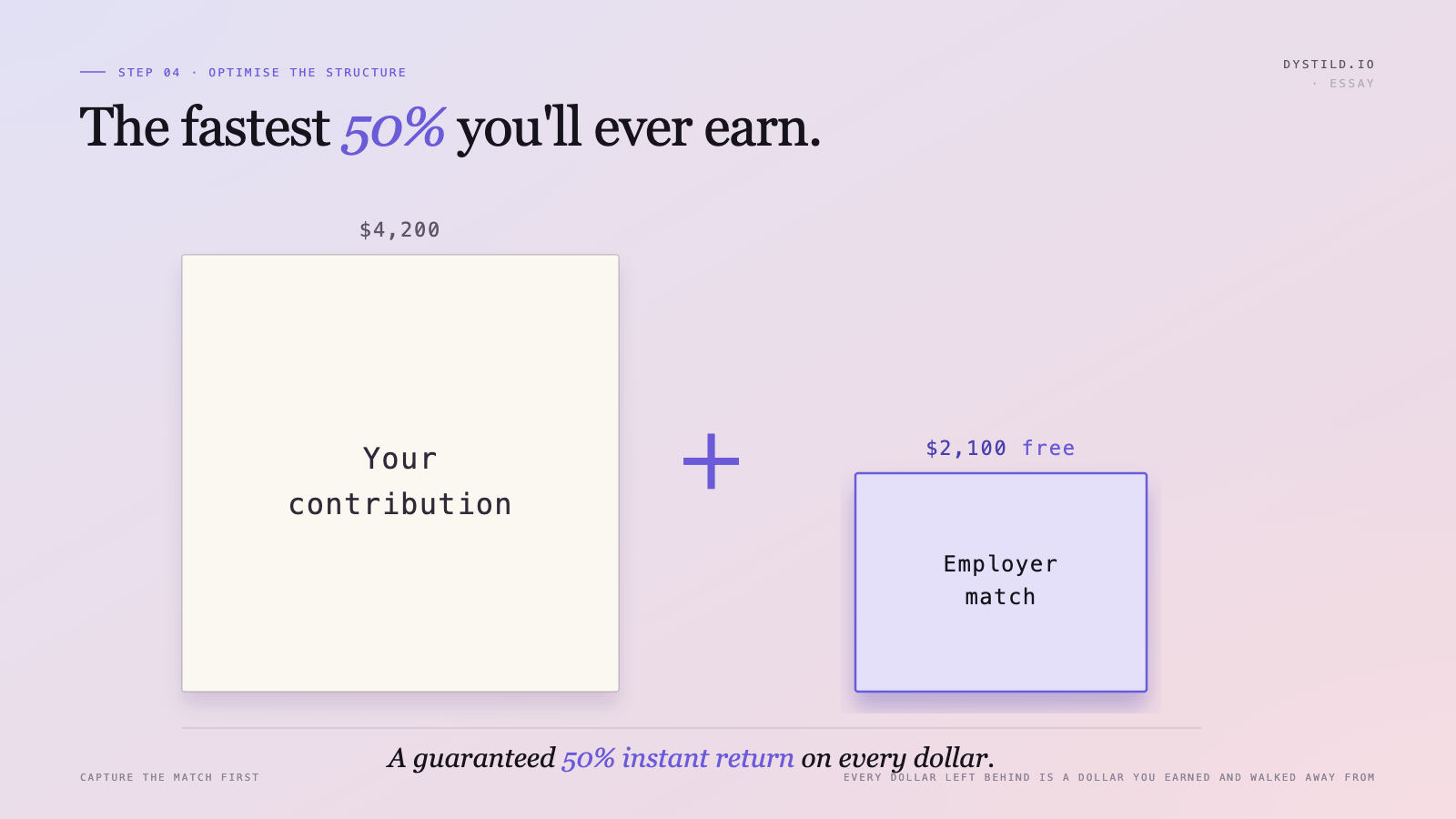

How it works

Most 401(k) plans come with some version of an employer match. A common structure: your employer matches 50% of your contributions up to 6% of your salary. So if you earn $70,000 and contribute 6% ($4,200), your employer puts in another $2,100. That $2,100 is yours — it's part of your compensation — but you only get it if you contribute enough to trigger it.

Contribute less than 6%, and you leave part of that match uncollected. Contribute nothing, and you leave all of it.

The 50% figure I used is just an example. Some employers match dollar-for-dollar. Some match a smaller percentage. The specific numbers don't matter much — what matters is whether you're contributing at least enough to get the full match your plan allows.

What people are actually leaving behind

A Vanguard analysis found that the average worker who doesn't capture their full match is leaving roughly $1,336 a year unclaimed. That's real compensation — the same as a raise — just structured differently.

$1,336 a year invested at a 7% average return over a 30-year career compounds to just over $142,000.

That's not a speculative number. That's what the match alone would grow to, separate from your own contributions, if you'd just taken what was being offered.

The part that makes it worse

Because this money goes into a retirement account, it grows tax-advantaged. A traditional 401(k) reduces your taxable income in the year you contribute, so the contribution costs you less than the face value. If you're in the 22% bracket, a $4,200 contribution reduces your tax bill by about $924 — meaning the effective out-of-pocket cost is closer to $3,276.

Your employer puts in $2,100 on top of that. You've contributed $3,276 of your own money and have $6,300 working for you. That's nearly a 100% return before a single dollar of market growth.

The match makes the 401(k) genuinely hard to beat as a first investment vehicle, at least up to the match threshold.

What to actually check

Most people don't know exactly how their match is structured. That's the first thing to fix.

Log into your HR system or your 401(k) provider's website — usually Fidelity, Vanguard, Empower, or similar. Find the plan summary. Look for the match formula. Then check what percentage of your salary you're currently contributing.

If you're contributing less than the threshold that triggers the full match, increase it. One change in your HR portal. You'll see a slightly smaller paycheck, but you'll be collecting compensation you're already owed.

If your company doesn't offer a match, or if you're self-employed, the math shifts — but there are still good reasons to use a retirement account. That's a longer conversation for another post.