April 21, 2026

·10 min read

How to Build Wealth: The 5-Step Framework

Most financial advice is a list of things you should do. Open a Roth IRA. Max your 401k. Build an emergency fund. Cut subscriptions. The advice isn't wrong — but presented as a flat list, it creates a problem: people jump to whichever step feels most interesting or most urgent, skip the ones that feel boring, and end up with a portfolio and no emergency fund, or a HYSA and credit card debt at 22%.

The steps aren't parallel. They're sequential. And the sequence is the part nobody explains.

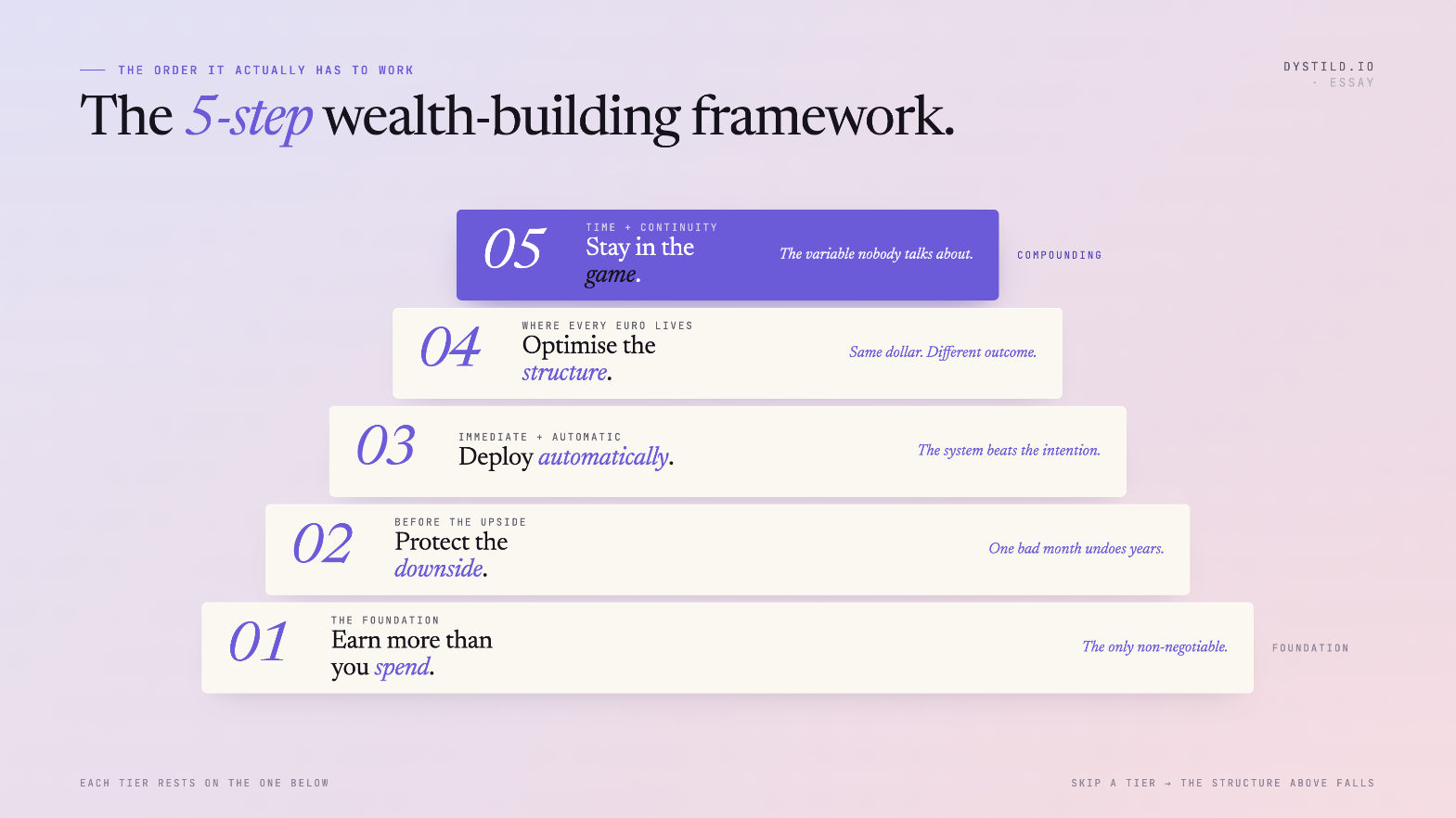

Here is the framework, in the order it actually has to work.

Step 1: Earn more than you spend

This is the only non-negotiable. Without a monthly surplus — some amount of money left after all expenses are paid — nothing else in this framework is possible. You cannot save what you don't have. You cannot invest what doesn't exist.

The surplus is the raw material for everything that follows.

What's worth understanding is that the surplus can be increased from two directions: cutting spending or growing income. Most personal finance advice focuses almost entirely on the spending side — the latte factor, subscription audits, cooking at home. That advice is not wrong, but it has a floor. There's a limit to how much you can cut before the cuts meaningfully reduce quality of life.

There's no ceiling on income. The highest-leverage financial decision most people make over a lifetime is not optimising their spending — it's growing their earning capacity through skills, career moves, or building something additional. A 10% income increase with flat spending is worth more than almost any investment optimisation.

That said: if spending is genuinely exceeding income, no investment strategy, tax optimisation, or account structure solves anything. Step 1 has to be in place before any other step has meaning.

Step 2: Protect the downside before building the upside

Once a surplus exists, the instinct is to start building — open an investment account, start putting money to work, let it grow. That instinct is wrong if certain foundations aren't in place first.

The scenarios that wipe out wealth in progress are more predictable than people think:

A single unexpected expense — a medical bill, a car repair, a job loss — without an emergency fund means that expense goes on a credit card at 20%+ interest. One month of bad luck undoes months of investment progress, and the credit card debt then compounds against you until it's paid off.

High-interest debt already in place erodes faster than investments build. Carrying $8,000 in credit card debt at 22% while investing in an index fund returning 7% is a net loss of 15% on that capital every year. The math is unambiguous — the debt has to go first.

Inadequate insurance means a catastrophic event (health crisis, disability, total loss of property) can eliminate everything built to that point. Insurance is not an investment. It is the thing that prevents the investment from being destroyed.

The correct order within this step: emergency fund first (start with $1,000, build to 3–6 months of essential expenses in a high-yield savings account), then eliminate high-interest debt aggressively, then verify insurance coverage is adequate.

Only once these are in place does the upside-building in steps 3–5 rest on solid ground.

Step 3: Put the surplus to work immediately and automatically

A surplus sitting in a checking account is not building wealth. It is sitting still, earning close to nothing, waiting to be spent. The transition from earning a gap to actually building wealth happens at the moment that surplus gets deployed into an account where it compounds.

Two words matter here equally: immediately and automatically.

Immediately because delay has a real cost. Every month a Roth IRA contribution doesn't happen is a month of compound growth that doesn't start. Every month cash sits in a checking account instead of a HYSA at 4% is money left on the table. There is no benefit to waiting.

Automatically because willpower is not a reliable financial system. The person who intends to transfer money to savings at the end of the month will transfer less — or nothing — more often than the person who automates the transfer the day after payday. The system is more durable than the intention. The best financial setup is one where the right thing happens by default, and doing the wrong thing requires an active decision to interrupt the automation.

The practical implementation is simple: set up automated transfers out of your checking account on payday. Emergency fund top-up first if not funded, 401k contribution already handled via payroll, then Roth IRA, then brokerage. What's left after those transfers is genuinely discretionary. Spend it without guilt — it's already what's left after the right things happened automatically.

Step 4: Maximise the return on every dollar through structure

This is the step that has the largest gap between how much it matters and how much attention most people pay to it.

Two people investing the same monthly amount, in the same index fund, with the same market returns, end up with dramatically different outcomes after 30 years based on one thing: which accounts they used.

The mechanisms that erode wealth silently:

Tax drag on a brokerage account. Dividends are taxed annually as ordinary income. Capital gains are taxed when you sell. Over 30 years, this drag compounds into a significant reduction of terminal value compared to the same money in a Roth IRA, where growth is never taxed.

Missed employer match. An employer who matches 401k contributions up to 4% of salary is offering a guaranteed 50–100% return on those dollars, depending on the match structure. Not contributing enough to capture the full match is declining that return every single paycheck. There is no investment that reliably beats a 100% guaranteed return.

Cash earning nothing. An emergency fund in a checking account at 0.01% instead of a HYSA at 4% costs real money every year. On $20,000, that's roughly $800 annually — for doing nothing except not opening the right account.

High-fee investment products. A fund with a 1% annual expense ratio versus one at 0.05% seems like a small difference. On $200,000 over 20 years, it represents tens of thousands of dollars in compounded drag.

None of these optimisations require more income, more discipline, or more risk tolerance. They require putting each dollar in the right account — which is a one-time decision with decades of compounding impact.

Step 5: Stay in the game long enough for compounding to work

Compounding is not a metaphor or a motivational concept. It is a specific mathematical mechanism that requires two inputs: time and continuity. Remove either one and the mechanism stops working.

The two behaviours that most reliably destroy compounding:

Early withdrawal. Taking money out of retirement accounts early — for emergencies, for purchases, for any reason — not only incurs the penalty and tax at the moment of withdrawal, it permanently removes that capital from decades of future compounding. The money you withdraw at 35 is not just the dollar amount — it is that amount multiplied by whatever the market would have returned between 35 and 65. The invisible cost is always larger than the visible one.

Stopping contributions during downturns. Market declines feel like a reason to pause investing. Mathematically, they are the opposite — they are the moments when each dollar buys more of an asset that will be worth more later. The investor who keeps contributing through a 30% market decline and the subsequent recovery ends up significantly ahead of the investor who paused and waited for confidence to return. The confidence almost always returns after the best recovery gains have already happened.

The underrated variable in long-term wealth building is not picking the right stocks, finding the right funds, or timing the market correctly. It is the decision to keep going when it feels uncomfortable — which it will, repeatedly, over any 30-year horizon.

Why the order matters more than any individual step

The reason this framework works as a sequence rather than a checklist is that each step creates the conditions for the next one to function properly.

Without step 1 there is no surplus to protect, deploy, or compound.

Without step 2, a single bad event destroys whatever steps 3–5 have built.

Without step 3, the surplus never gets deployed — good intentions don't compound.

Without step 4, money is deployed into suboptimal structures that quietly erode returns.

Without step 5, the compounding in step 4 never reaches its potential.

Most people skip to step 4 or 5 — portfolio optimisation, investment selection — without having steps 1 and 2 solidly in place. The result is a sophisticated investment strategy sitting on an unstable foundation. One emergency, one credit card balance, one missed employer match undoes the sophistication entirely.

The framework applied to a single month looks like this:

- —Income arrives

- —Essential expenses paid

- —Automated transfer to HYSA (emergency fund, if not yet funded)

- —401k contribution via payroll (at minimum, enough for full match)

- —Automated Roth IRA contribution

- —Remainder to brokerage or specific goals

- —Whatever is left is genuinely discretionary

Nothing in that sequence requires a decision after it is set up. It runs automatically. That is the point — not because financial decisions are too hard to make, but because removing the decision removes the opportunity to make the wrong one.

The sophistication is not in the investments. It is in the system.